So far, we have seen how to cluster objects using \(k\)-means:

Start with an initial set of cluster centers,

Assign each object to its closest cluster center

Recompute the centers of the new clusters

Repeat 2 \(\rightarrow\) 3 until convergence

In \(k\)-means clustering every object is assigned to a single cluster.

This is called hard assignment.

However, there may be cases where we either cannot use hard assignments or we do not want to do it.

In particular, we might have reason to believe that the best description of the data is a set of overlapping clusters.

Overlapping Clusters

Income Level Example

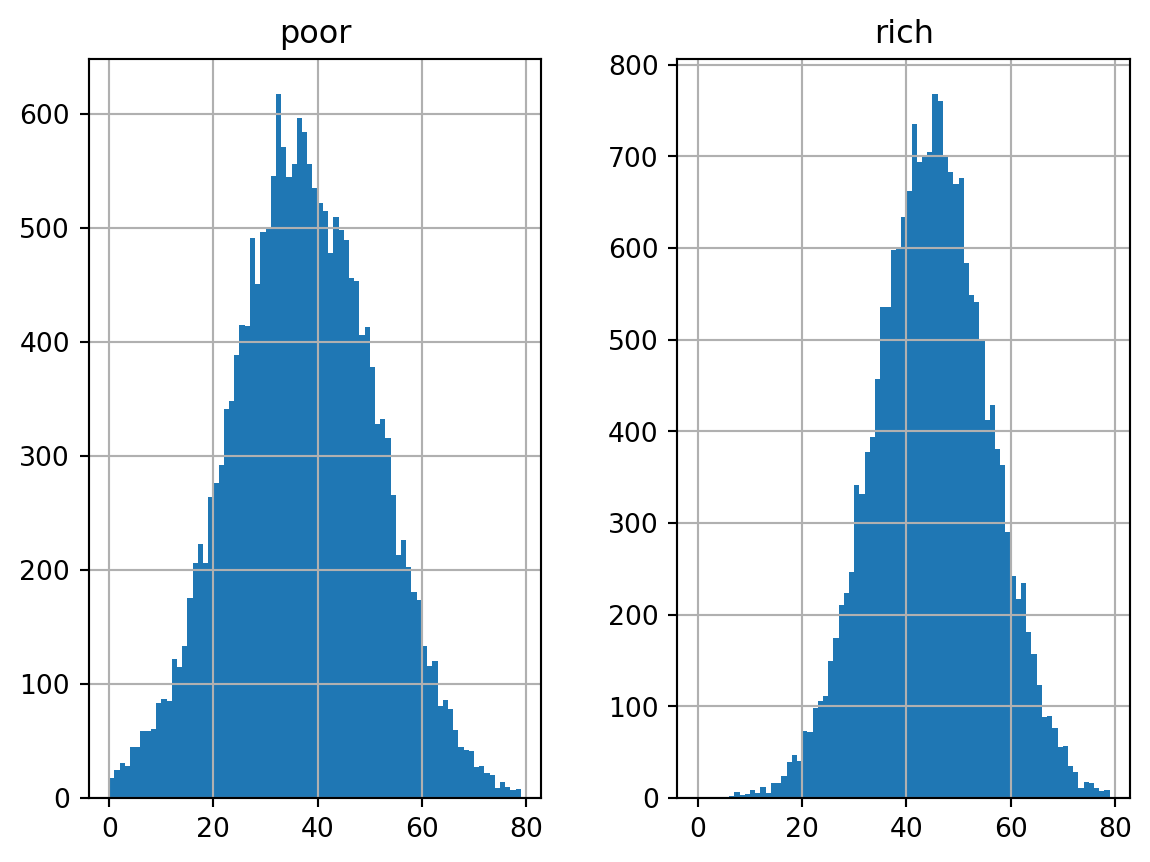

Consider a population in terms of a simple binary income level: higher or lower than some threshold.

How might we model such a population in terms of the single feature age?

Income Level Sampling

Let’s sample 20,000 above income threshold individuals and 20,000 below income threshold individuals.

From this sample we get have the following histograms.

Code

# original inspiration for this example from# https://www.cs.cmu.edu/~./awm/tutorials/gmm14.pdffrom scipy.stats import multivariate_normalnp.random.seed(4)df = pd.DataFrame(multivariate_normal.rvs(mean = np.array([37, 45]), cov = np.diag([196, 121]), size =20000), columns = ['below', 'above'])df.hist(bins =range(80), sharex =True, sharey=True, figsize=(12, 2))plt.show()

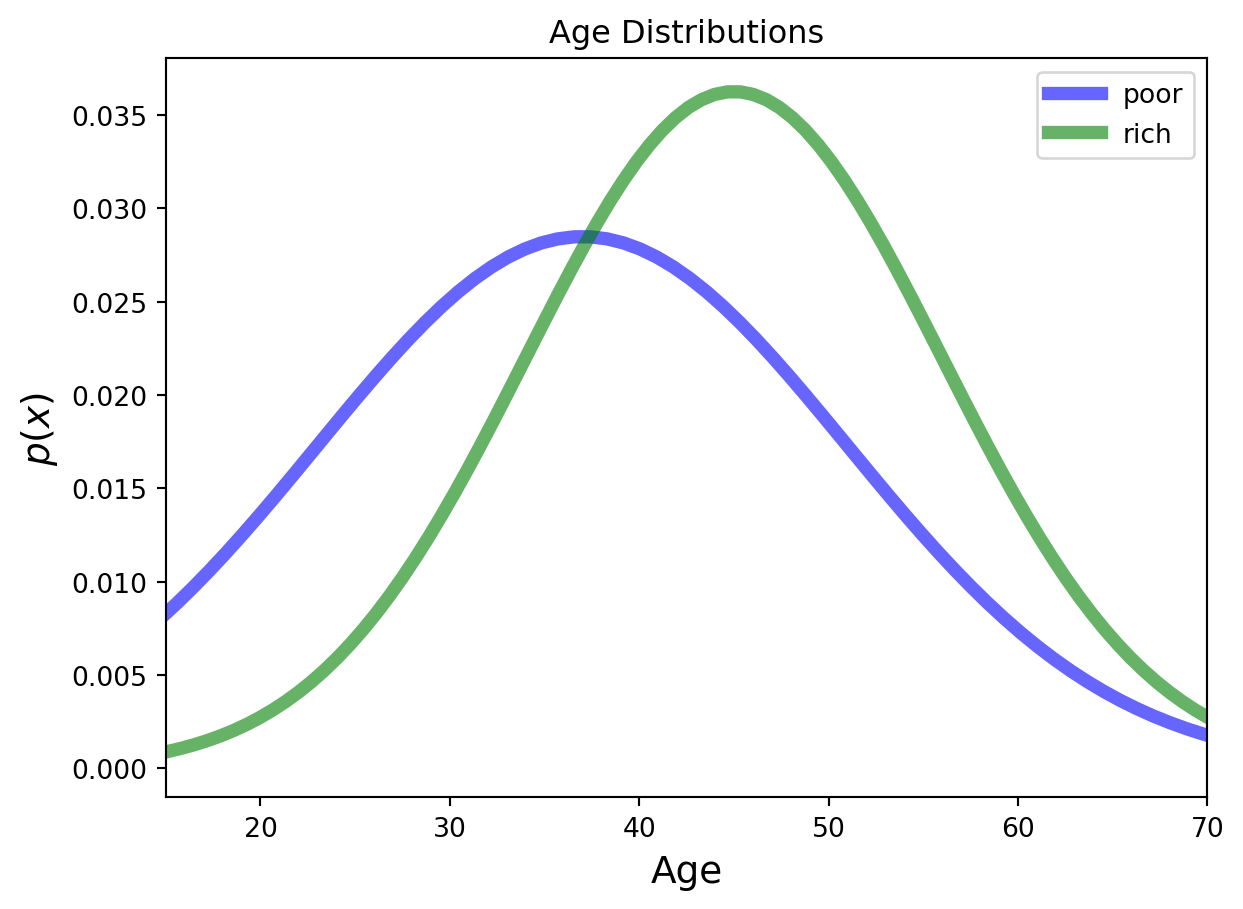

We find that ages of the below income threshold set have mean \(\mu=37\) with standard deviation \(\sigma=14\), while the ages of the above income threshold set have mean \(\mu=45\) with standard deviation \(\sigma=11\).

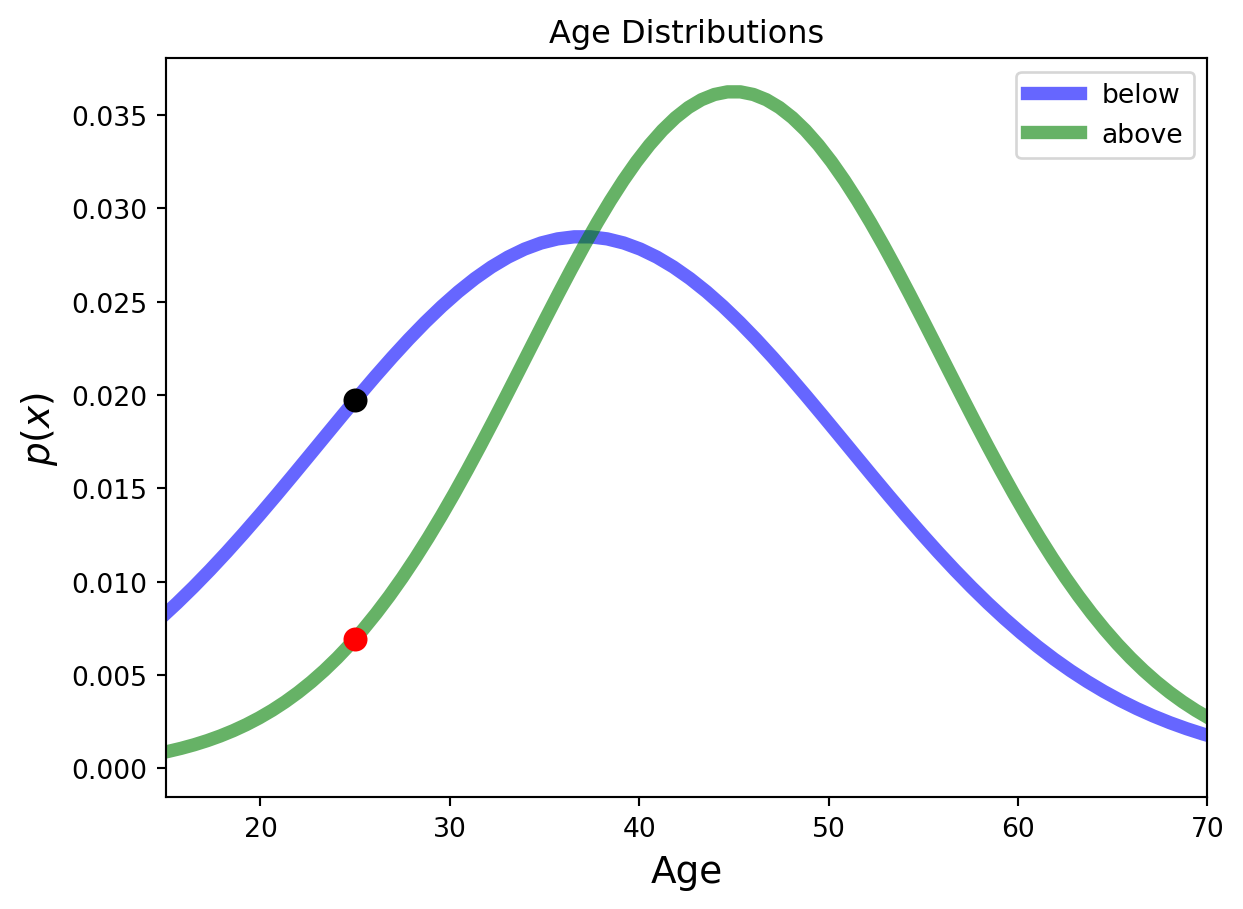

Income Level by Age

We can plot gaussian distributions for the two income levels.

Code

from scipy.stats import normplt.figure(figsize=(7, 4.5))x = np.linspace(norm.ppf(0.001, loc =37, scale =14), norm.ppf(0.999, loc =37, scale =14), 100)plt.plot(x, norm.pdf(x, loc =37, scale =14),'b-', lw =5, alpha =0.6, label ='below')x = np.linspace(norm.ppf(0.001, loc =45, scale =11), norm.ppf(0.999, loc =45, scale =11), 100)plt.plot(x, norm.pdf(x, loc =45, scale =11),'g-', lw =5, alpha =0.6, label ='above')plt.xlim([15, 70])plt.xlabel('Age', size=14)plt.legend(loc ='best')plt.title('Age Distributions')plt.ylabel(r'$p(x)$', size=14)plt.show()

Soft Clustering

two overlapping clusters.

given some particular individual at a given age, say 25, we cannot say for sure which cluster they belong to.

use probability to quantify our uncertainty about cluster membership.

Individual belongs to the cluster 1 with some probability \(p_1\) and the cluster 2 with a different probability \(p_2\).

Naturally we expect the probabilities to sum up to 1.

This is called soft assignment, and a clustering using this principle is called soft clustering.

Conditional Probability

More formally, we say that an object can belong to each particular cluster with some probability, such that the sum of the probabilities adds up to 1 for each object.

For example, assuming that we have two clusters \(C_1\) and \(C_2\), we can have that an object \(x_1\) belongs to \(C_1\) with probability \(0.3\) and to \(C_2\) with probability \(0.7\).

Note that the distribution over \(C_1\) and \(C_2\) only refers to object \(x_1\).

Maximum likelihood estimation is a method to estimate the parameters of a probability distribution given a sample of observed data that best fits the data.

Likelihood Function

The likelihood function \(L(\boldsymbol{\theta}, x)\) represents the probability of observing the given data \(x\) as a function of the parameters \(\boldsymbol{\theta}\) of the distribution.

The primary purpose of the likelihood function is to estimate the parameters that make the observed data \(x\) most probable.

The likelihood function for a set of samples \(x_{n}~\text{for}~n=1, \ldots, N\) drawn from an independent and identically distributed (i.i.d.) Gaussian distribution is

For a particular set of parameters \(\mu, \sigma^{2}\)

large values of \(L(\mu, \sigma^{2}, x_1, \ldots, x_n)\) indicate the observed data is very probable (high likelihood) and thus well modeled by the parameters

small values of \(L(\mu, \sigma^{2}, x_1, \ldots, x_n)\) indicate the observed data is very improbable (low likelihood) and thus poorly modeled by the parameters

The parameters that maximize the likelihood function are called the maximum likelihood estimates.

Log-likelihood

A common manipulation to obtain a more useful form of the likelihood function is to take its natural logarithm.

Advantages of the log-likelihood:

The log function is monotonically increasing, so the MLE is the same as the log-likelihood estimate

The product of probabilities becomes a sum of logarithms, which is more numerically stable

Using the log-likelihood we will be able to derive formulas for the maximum likelihood estimates.

Maximizing the log-likelihood

How do we maximize (optimize) a function of parameters?

To find the optimal parameters of a function, we compute partial derivatives of the function and set them equal to zero. The solution to these equations gives us a local optimal value for the parameters.

The full derivation of these results is provided here.

Tip: Try deriving these results yourself!

Summary of MLE

Given samples \(x_{1}, \ldots, x_n\) drawn from a Gaussian distribution, we compute the maximum likelihood estimates by maximizing the log likelihood function

We use this information to help our understanding of Gaussian Mixture models.

Gaussian Mixture Models

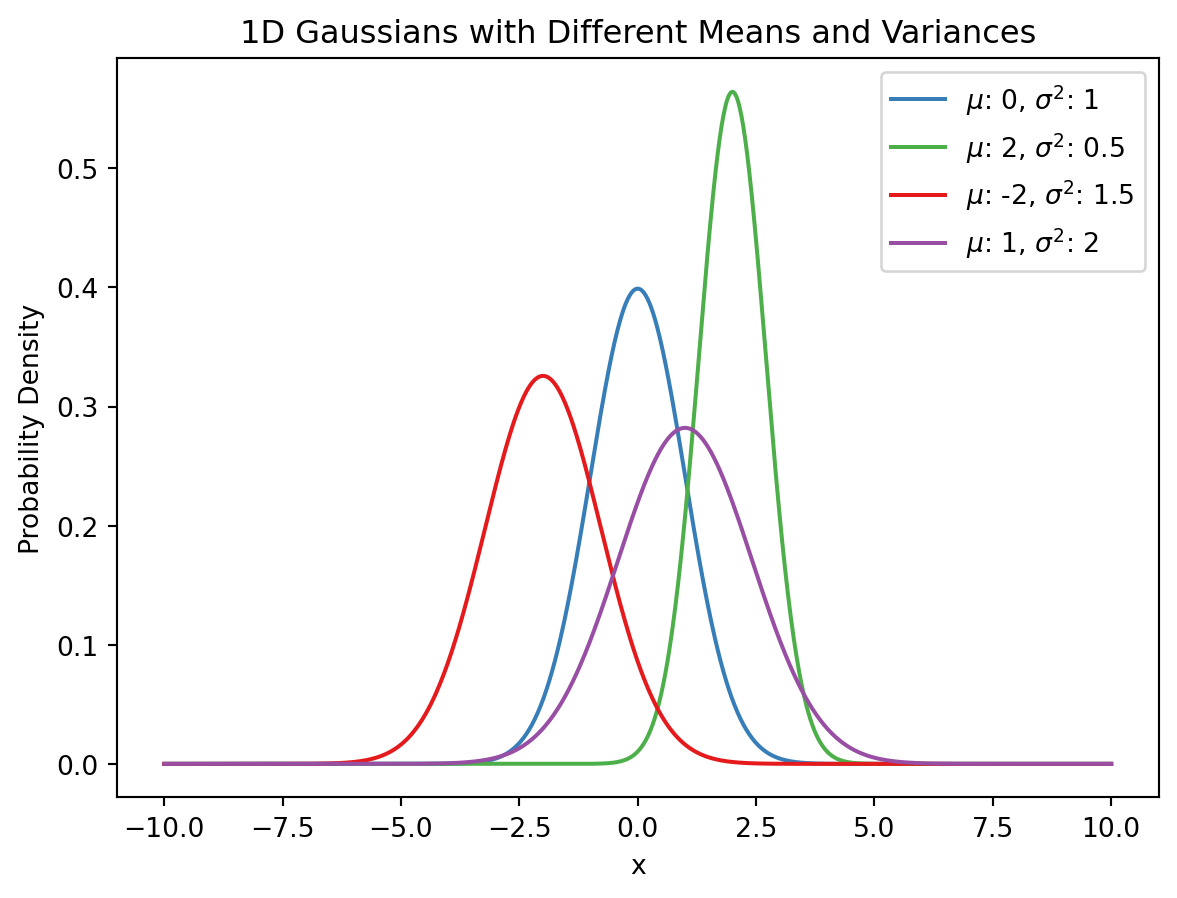

Univariate Gaussians

In GMMs we assume that each of our clusters follows a Gaussian (normal) distribution with their own parameters.

Code

import numpy as npimport matplotlib.pyplot as plt# Define the parameters for the 4 Gaussiansparams = [ {"mean": 0, "variance": 1, "color": "#377eb8"}, # Blue {"mean": 2, "variance": 0.5, "color": "#4daf4a"}, # Green {"mean": -2, "variance": 1.5, "color": "#e41a1c"}, # Red {"mean": 1, "variance": 2, "color": "#984ea3"} # Purple]# Generate x valuesx = np.linspace(-10, 10, 1000)# Plot each Gaussianfor param in params: mean = param["mean"] variance = param["variance"] color = param["color"]# Calculate the Gaussian y = (1/ np.sqrt(2* np.pi * variance)) * np.exp(- (x - mean)**2/ (2* variance))# Plot the Gaussian plt.plot(x, y, color=color, label=f"$\\mu$: {mean}, $\\sigma^2$: {variance}")# Add legendplt.legend()# Add title and labelsplt.title("1D Gaussians with Different Means and Variances")plt.xlabel("x")plt.ylabel("Probability Density")# Show the plotplt.show()

This is a similar situation to our previous example where we considered labeling a person as above or below an income threshold based on the single feature age.

This could be a hypothetical situation with \(K=4\) normally distributed clusters.

Multivariate Gaussians

Given data points \(\mathbf{x}\in\mathbb{R}^{d}\), i.e., \(d\)-dimensional points, then we use the multivariate Gaussian to describe the clusters. The formula for the multivariate Gaussian is

where \(\Sigma\in\mathbb{R}^{d\times d}\) is the covariance matrix, \(\vert \Sigma\vert\), denote the determinant of \(\Sigma\), and \(\boldsymbol{\mu}\) is the \(d\)-dimensional vector of expected values.

The covariance matrix is the multidimensional analog of the variance. It determines the extent to which vector components are correlated.

See here for a refresher on the covariance matrix.

Notation

The notation \(x \sim \mathcal{N}(\mu, \sigma^2)\) is used to denote a univariate random variable that is normally distributed with expected value \(\mu\) and variance \(\sigma^{2}.\)

The notation \(\mathbf{x} \sim \mathcal{N}(\boldsymbol{\mu}, \Sigma)\) is used to denote a multivariate random variable that is normally distributed with mean \(\boldsymbol{\mu}\) and covariance matrix \(\Sigma\).

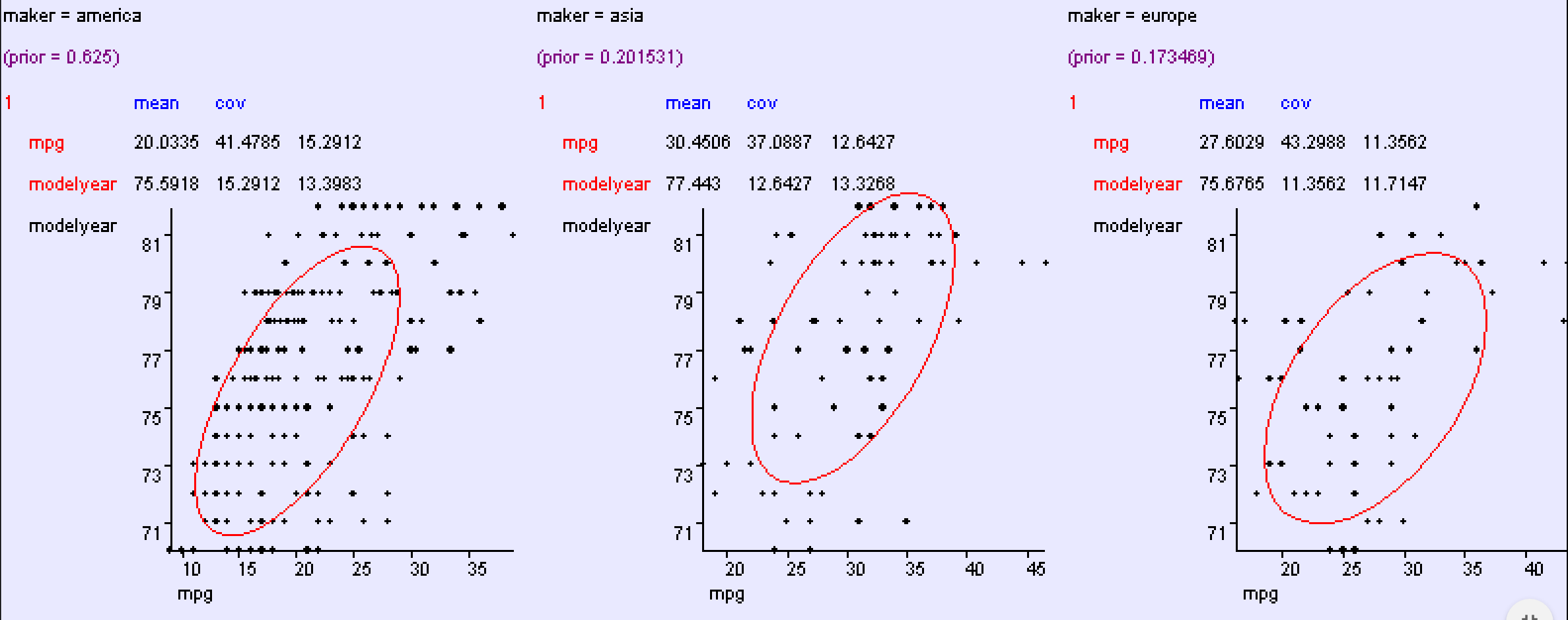

Multivariate Example: Cars

To illustrate a particular model, let us consider the properties of cars produced in the US, Europe, and Asia.

For example, let’s say we are looking to classify cars based on their model year and miles per gallon (mpg).

It seems that the data can be described (roughly) as a mixture of threemultivariate Gaussian distributions.

Expectation-Maximization for Gaussian Mixture Models

The Clustering Problem

Suppose we observe \(n\) data points \(X = \{x_1, x_2, \ldots, x_n\}\) in \(\mathbb{R}^d\) that appear to come from multiple clusters.

We want to model this data as a mixture of \(K\) Gaussian distributions, each representing a different cluster.

The Gaussian Mixture Model

A Gaussian Mixture Model (GMM) assumes each data point is generated by the following process:

Choose a cluster \(k \in \{1, 2, \ldots, K\}\) with probability \(\pi_k\) (where \(\sum_{k=1}^K \pi_k = 1\))

Generate the point from a Gaussian distribution: \(x_i \sim \mathcal{N}(\mu_k, \Sigma_k)\)

The probability density of observing point \(x_i\) is:

E-Step: Since we don’t know \(z_i\), we compute the expected value of the indicator \(\mathbb{1}(z_i = k)\), which is the posterior probability \(\gamma_{ik} = p(z_i = k \mid x_i, \theta^{(t)})\), where \(\theta^{(t)}\) is the parameter vector at iteration \(t\).

M-Step: With these soft assignments, maximizing the expected complete log-likelihood yields closed-form updates that look like weighted versions of the standard MLE formulas

This elegant approach transforms an intractable optimization problem into a simple iterative procedure with intuitive updates at each step.

We observe data points \(x_1, x_2, \ldots, x_n\) in \(d\)-dimensional space

We assume the data comes from \(K\) Gaussian distributions, each with mean \(\mu_k\), covariance \(\Sigma_k\), and mixing weight \(\pi_k\)

The latent variables are the cluster assignments \(z_i\) (which component generated each point)

Goal: Find parameters \(\theta = \{\mu_k, \Sigma_k, \pi_k\}_{k=1}^K\) that maximize the likelihood of the observed data

Initialization

Randomly initialize the \(K\) means \(\mu_k\) (or use k-means clustering)

Initialize covariances \(\Sigma_k\) (often as identity matrices or sample covariance)

Initialize mixing weights \(\pi_k = \frac{1}{K}\) (uniform distribution over components)

E-Step: Compute Responsibilities

For each data point \(x_i\) and each component \(k\), compute the responsibility \(\gamma_{ik}\) (the probability that point \(i\) belongs to component \(k\) given current parameters)

Each parameter update has an intuitive interpretation as a weighted MLE

Iteration and Convergence

Alternate between E and M steps until convergence

Monitor the log-likelihood: it’s guaranteed to increase (or stay the same) at each iteration

Stop when log-likelihood change falls below a threshold or after a maximum number of iterations

Note: EM finds a local maximum, so results depend on initialization (run multiple times with different initializations)

Key Intuition

E-step: Given current cluster parameters, probabilistically assign points to clusters

M-step: Given these soft assignments, update cluster parameters as if they were the true assignments

This 🐓 and 🥚 problem is resolved through iteration

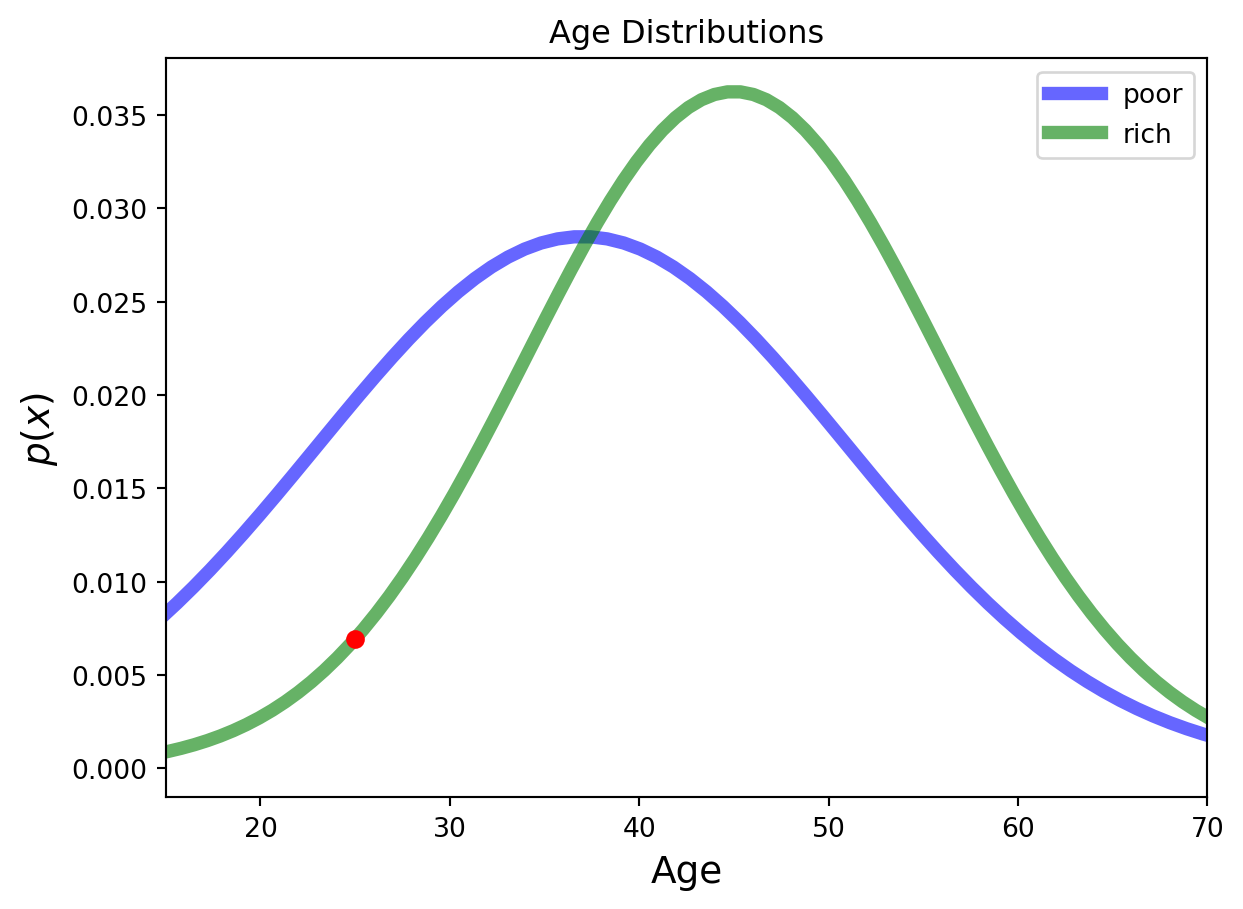

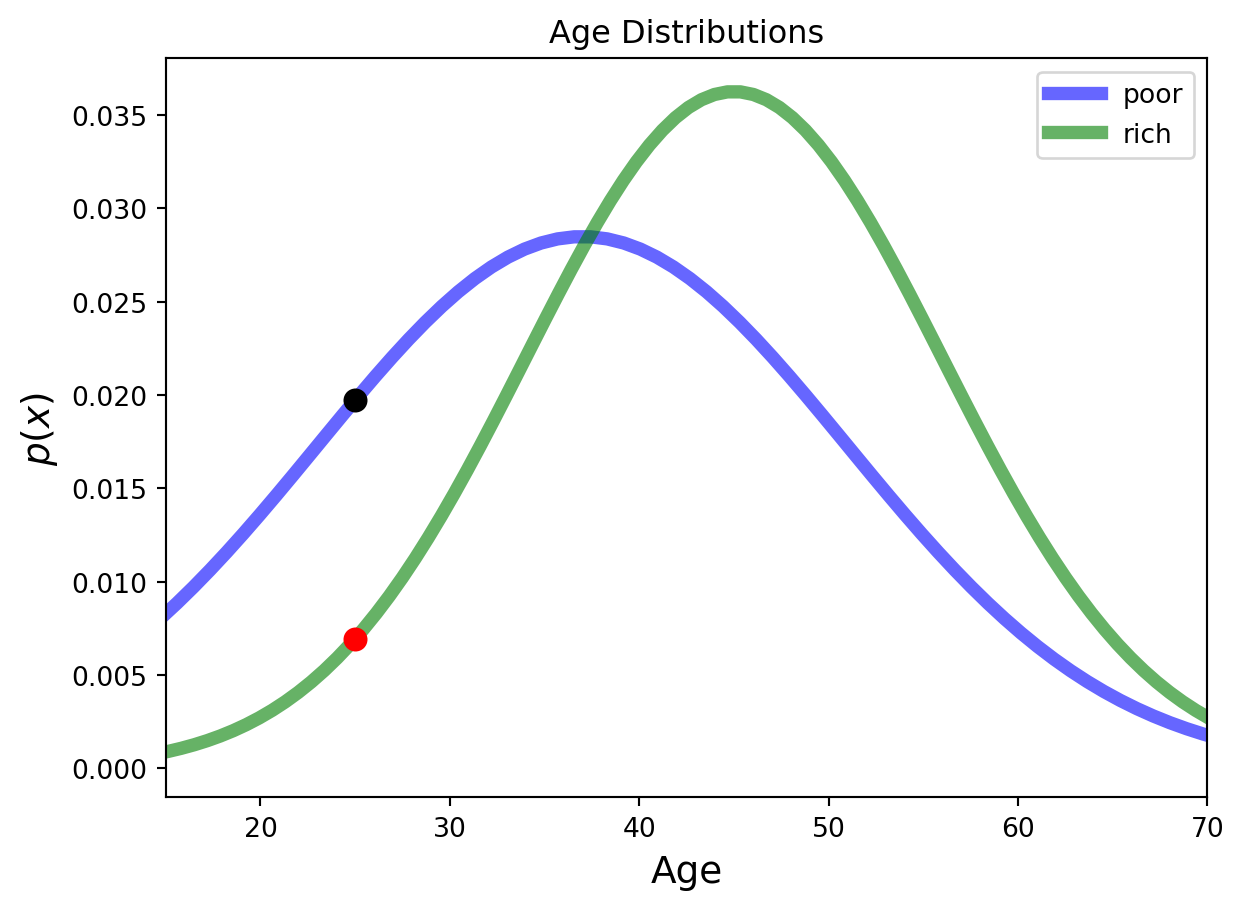

Income Level Example

We have

Our single data point \(x=25\), and

We have 2 Gaussians representing our clusters,

\(C_1\) with parameters \(\mu_1 = 37, \sigma_1^{2}=14\) and

\(C_2\) with parameters \(\mu_2 = 45, \sigma_2^{2}=11\),

Our latent variables are the probabilities that we classify someone as either above or below an income threshold, i.e., \[

\gamma_1 = P(z = 1) = P(\text{above income threshold})

\] and \[

\gamma_2 = P(z = 2) = P(\text{below income threshold}).

\]

Income Level Example, cont.

Our interest in this problem is computing the posterior probability, which is,

“red” = \(P(\text{age 25} | \text{above})\) and “black” = \(P(\text{age 25} | \text{below})\), and

\(P(\text{above})\) and \(P(\text{below})\) are the prior probabilities (mixing weights) that must sum to 1: \(P(\text{above}) + P(\text{below}) = 1\),

e.g. 0.5 in this example since we split the 20K points equally.

Convergence criteria

The convergence criteria for the Expectation-Maximization (EM) algorithm assess the change across iterations of either the

likelihood function, or

model parameters

with usually a limit on the maximum number of iterations.

\(\theta^{(t)}\) represents the model parameters (means, covariances, and weights) at iteration \(t\),

\(||\cdot||_2\) is the Euclidean (L2) norm,

\(\text{tol}\) is a small positive number.

Maximum Number of Iterations

The EM algorithm is typically capped at a maximum number of iterations to avoid long runtimes in cases where the log-likelihood or parameters converge very slowly or never fully stabilize.

\[

t > \text{max\_iterations}

\]

Where:

\(\text{max\_iterations}\) is a predefined limit (e.g., 100 or 500 iterations).

Storage and Computational Costs

It is important to be aware of the computational costs of our algorithm.

Storage costs:

There are \(N\)\(d\)-dimensional points

There are \(K\) clusters

There are \(N\times K\) coefficients \(r_{nk}\)

There are \(K\)\(d\)-dimensional cluster centers \(\boldsymbol{\mu}_k\)

There are \(K\)\(d\times d\) covariance matrices \(\Sigma_k\)

There are \(K\) weights \(w_k\)

Computational costs:

Computing each \(r_{nk}\) requires a sum of \(K\) evaluations of the Gaussian PDF.

Updating \(\gamma_k\) requires a division (though we must compute \(N_k\))

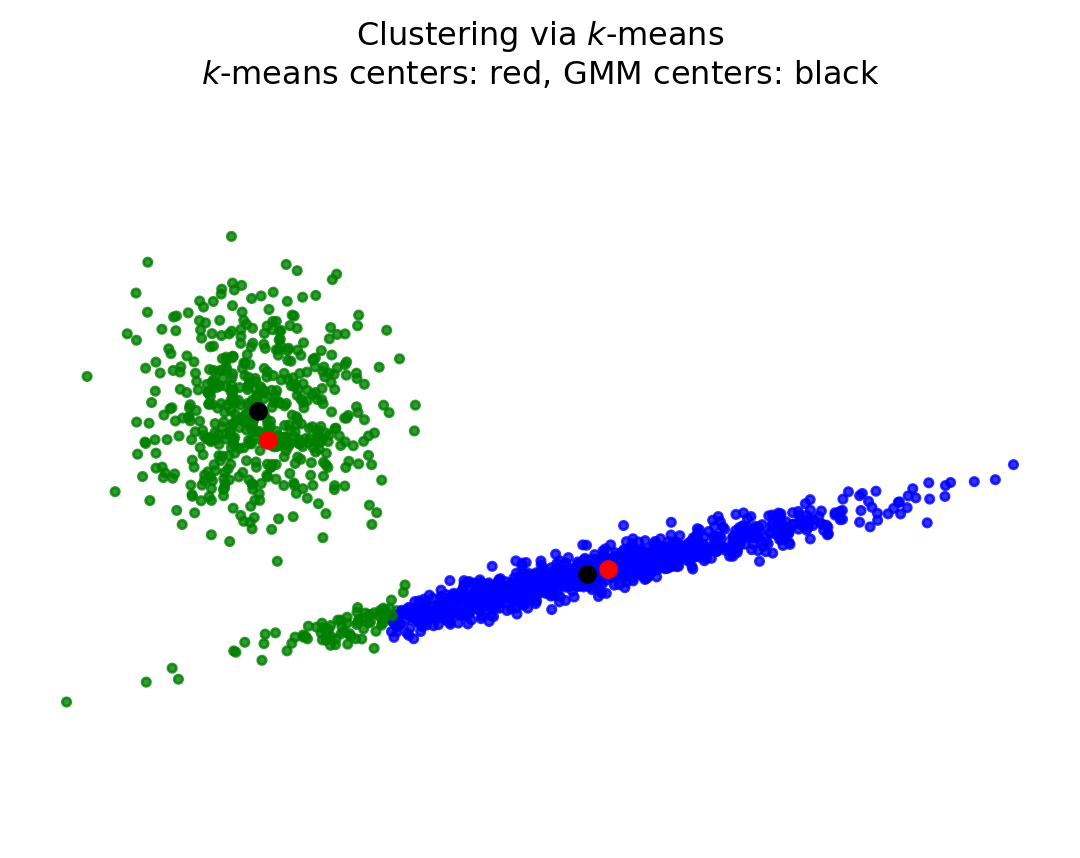

k-means vs GMMs

Let’s pause for a minute and compare GMM/EM with \(k\)-means.

GMM/EM

Initialize randomly or using some rule

Compute the probability that each point belongs in each cluster

Update the clusters (weights, means, and variances).

Repeat 2-3 until convergence.

\(k\)-means

Initialize randomly or using some rule

Assign each point to a single cluster

Update the clusters (means).

Repeat 2-3 until convergence.

From a practical standpoint, the main difference is that in GMMs, data points do not belong to a single cluster, but have some probability of belonging to each cluster.

In other words, as stated previously, GMMs use soft assignment.

For that reason, GMMs are also sometimes called soft \(k\)-means.

However, there is also an important conceptual difference.

The GMM starts by making an explicit assumption about how the data were generated.

It says: “the data came from a collection of multivariate Gaussians.”

We made no such assumption when we came up with the \(k\)-means problem. In that case, we simply defined an objective function and declared that it was a good one.

Nonetheless, it appears that we were making a sort of Gaussian assumption when we formulated the \(k\)-means objective function. However, it wasn’t explicitly stated.

The point is that because the GMM makes its assumptions explicit, we can

examine them and think about whether they are valid, and

replace them with different assumptions if we wish.

For example, it is perfectly valid to replace the Gaussian assumption with some other probability distribution. As long as we can estimate the parameters of such distributions from data (e.g., have MLEs), we can use EM in that case as well.

Versatility of EM

A final statement about EM generally. EM is a versatile algorithm that can be used in many other settings. What is the main idea behind it?

Notice that the problem definition only required that we find the clusters, \(C_i\), meaning that we were to find the \((\mu_i, \Sigma_i)\).

However, the EM algorithm posited that we should find as well the \(P(C_j|x_i) = P(z=j | x_i)\), that is, the probability that each point is a member of each cluster.

This is the true heart of what EM does.

By adding parameters to the problem, it actually finds a way to make the problem solvable.

These are the latent parameters we introduced earlier. Latent parameters don’t show up in the solution.

Examples

Example 1

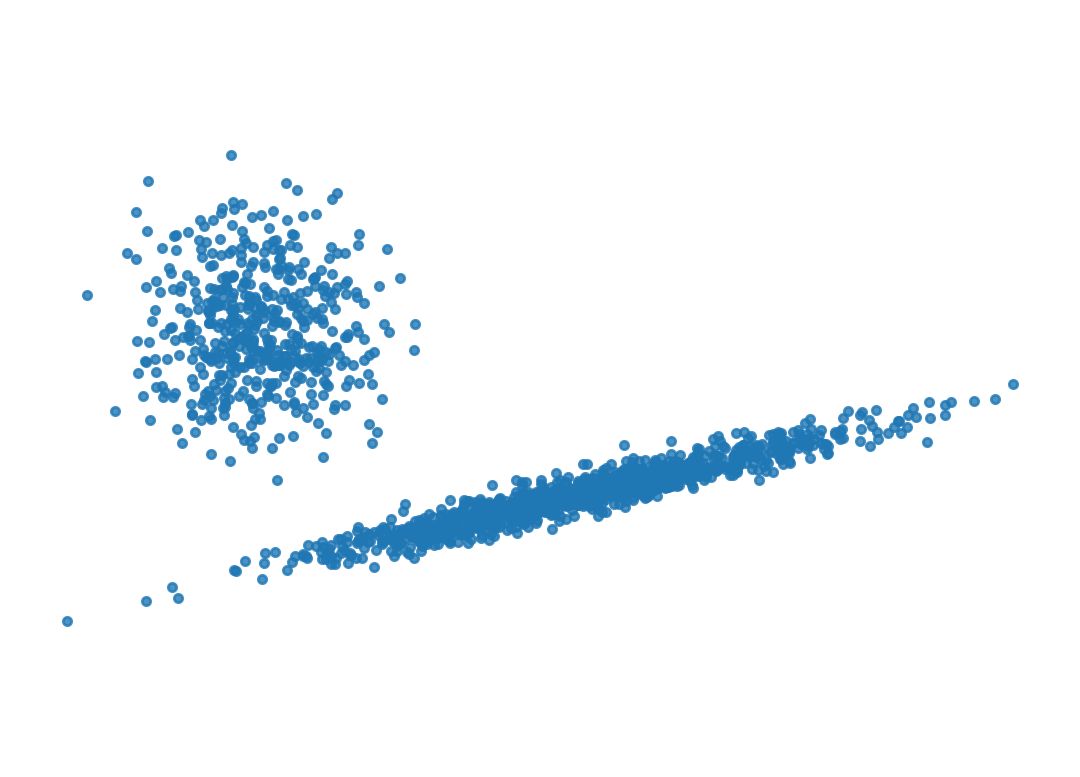

Here is an example using GMM.

We’re going to create two clusters, one spherical, and one highly skewed.

Code

# Number of samples of larger componentn_samples =1000# C is a transfomation that will make a heavily skewed 2-D GaussianC = np.array([[0.1, -0.1], [1.7, .4]])print(f'The covariance matrix of our skewed cluster will be:\n{C.T@C}')

The covariance matrix of our skewed cluster will be:

[[2.9 0.67]

[0.67 0.17]]

Code

import warningswarnings.filterwarnings('ignore')rng = np.random.default_rng(0)# now we construct a data matrix that has n_samples from the skewed distribution,# and n_samples/2 from a symmetric distribution offset to position (-4, 2)X = np.r_[(rng.standard_normal((n_samples, 2)) @ C),.7* rng.standard_normal((n_samples//2, 2)) + np.array([-4, 2])]

Code

plt.scatter(X[:, 0], X[:, 1], s =10, alpha =0.8)plt.axis('equal')plt.axis('off')plt.show()

Code

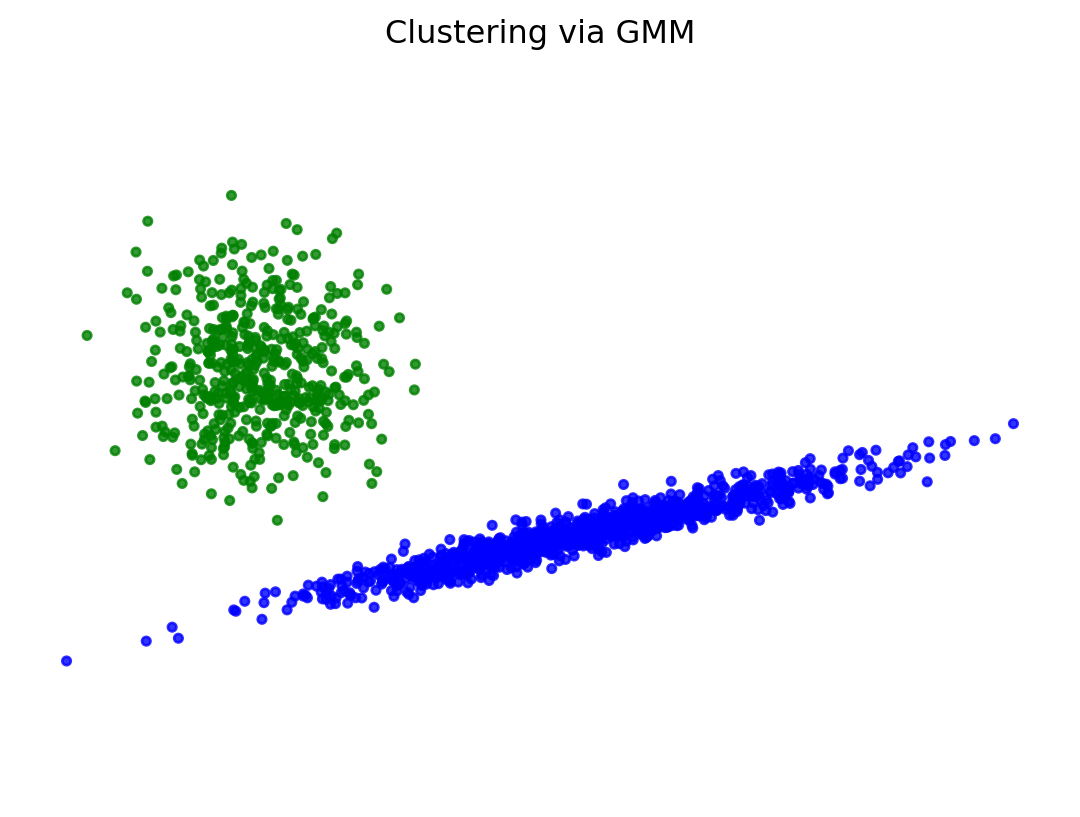

# Fit a mixture of Gaussians with EM using two componentsimport sklearn.mixturegmm = sklearn.mixture.GaussianMixture(n_components=2, covariance_type='full', init_params ='kmeans')y_pred = gmm.fit_predict(X)

Code

colors = ['bg'[p] for p in y_pred]plt.title('Clustering via GMM')plt.axis('off')plt.axis('equal')plt.scatter(X[:, 0], X[:, 1], color = colors, s =10, alpha =0.8)plt.show()

Code

for clus inrange(2):print(f'Cluster {clus}:')print(f' weight: {gmm.weights_[clus]:0.3f}')print(f' mean: {gmm.means_[clus]}')print(f' cov: \n{gmm.covariances_[clus]}\n')

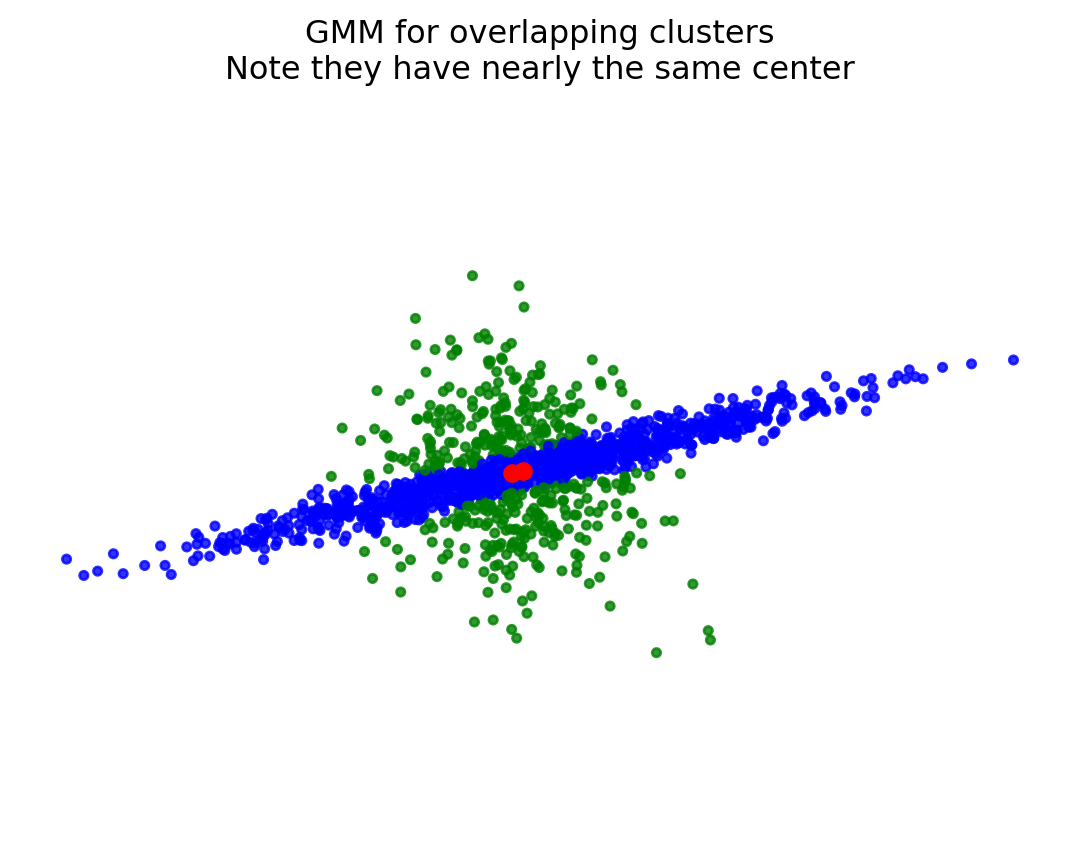

colors = ['bgrky'[p] for p in y_pred_over]plt.title('GMM for overlapping clusters\nNote they have nearly the same center')plt.scatter(X[:, 0], X[:, 1], color = colors, s =10, alpha =0.8)plt.axis('equal')plt.axis('off')plt.plot(gmm.means_[:,0], gmm.means_[:,1], 'ro')plt.show()

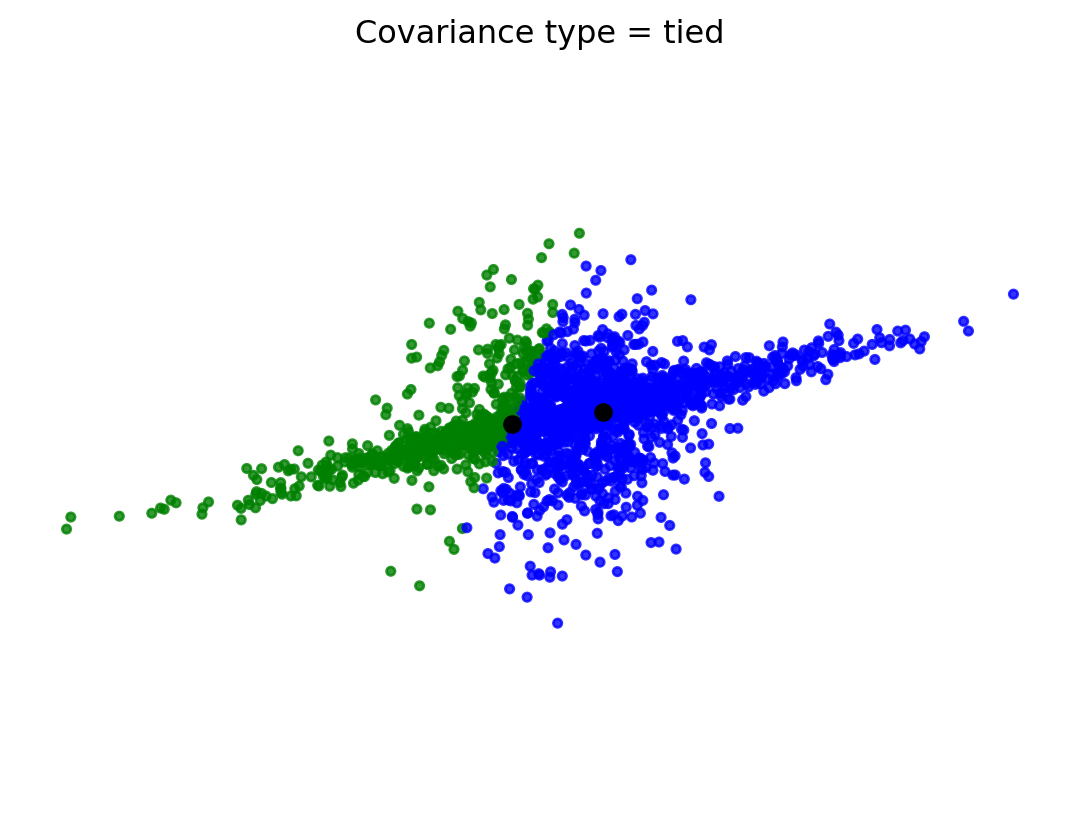

colors = ['bgrky'[p] for p in y_pred]plt.scatter(X[:, 0], X[:, 1], color=colors, s=10, alpha=0.8)plt.title('Covariance type = tied')plt.axis('equal')plt.axis('off')plt.plot(gmm.means_[:,0],gmm.means_[:,1], 'ok')plt.show()

Non-Skewed Clusters

Perhaps you believe in even more restricted shapes: all clusters should have their axes aligned with the coordinate axes.

That is, clusters are not skewed.

Then you only need to estimate the diagonals of the covariance matrices - just \(Kd\) parameters.

This is specified by the GMM parameter covariance_type='diag'.

colors = ['bgrky'[p] for p in y_pred]plt.scatter(X[:, 0], X[:, 1], color = colors, s =10, alpha =0.8)plt.axis('equal')plt.axis('off')plt.plot(gmm.means_[:,0], gmm.means_[:,1], 'oc')plt.show()

Round Clusters

Finally, if you believe that all clusters should be round, then you only need to estimate the \(K\) variances.

This is specified by the GMM parameter covariance_type='spherical'.

colors = ['bgrky'[p] for p in y_pred]plt.scatter(X[:, 0], X[:, 1], color = colors, s =10, alpha =0.8)plt.axis('equal')plt.axis('off')plt.plot(gmm.means_[:,0], gmm.means_[:,1], 'oc')plt.show()